Nitrogen fertilizer has become one of the most strategically important and financially dangerous inputs in modern agriculture.As explored in our previous articles on the global nitrogen fertilizer crisis and fertilizer logistics disruption, the market is being reshaped by rising urea prices, geopolitical instability, energy market volatility, and increasingly fragile global supply chains.

Reuters reported that in April 2026 India received urea offers clustered around $1,000 per metric ton, with some bids reaching $1,136 per ton. India ultimately contracted imports at $935–959 per ton, compared with $508–512 per ton only two months earlier [1].

But unlike many other industrial inputs, fertilizer is not optional.

For most field crops, nitrogen directly determines yield potential. And yield is not only the foundation of farm profitability, it is the foundation of global food production itself.

This is why the fertilizer crisis extends far beyond agriculture.

When fertilizer prices rise dramatically while grain prices remain under pressure, entire farming businesses become economically vulnerable. Farmers are squeezed between volatile input costs and commodity markets they cannot control. And increasingly, many operations simply cannot absorb the pressure any longer.

The consequences are already visible. In the United States, more farmers filed for bankruptcy in the first quarter of 2025 than in any full year since 2021 [2].

At the same time, rising input costs are increasingly affecting day-to-day production decisions. A recent nationwide survey conducted by the American Farm Bureau Federation among more than 5,700 producers found that around 70% of U.S. farmers report they cannot afford to purchase all the fertilizer they need for the season [3].

And this is not only a farm-sector problem.

If farms reduce production, delay planting, cut fertilizer rates, or leave acreage idle, less food ultimately reaches the market. The result is pressure across the entire food supply chain from grain availability and livestock feed to food prices for consumers.

And this is no longer a theoretical risk. International institutions are already warning that sustained fertilizer inflation is beginning to influence planting decisions and future food affordability. The FAO reported that rising fertilizer costs are contributing to expectations of reduced wheat acreage in 2026, as some producers shift toward less input-intensive crops [4].

Looking further ahead, the FAO warns that if high input costs persist and farmers continue producing with fewer inputs, lower yields later this year and into 2027 could translate into higher food commodity prices and retail food inflation for several years [5].

The World Bank has also warned that the current commodity environment could intensify this pressure: fertilizer prices are projected to rise further in 2026, driven by urea costs, increasing the risk of weaker agricultural output, additional inflation, and worsening food insecurity. Under prolonged disruption scenarios, millions more people could face acute food insecurity globally [6].

In other words, the nitrogen fertilizer crisis affects not only agriculture. It affects food security itself.

So the key question becomes: How can farming businesses survive and continue producing profitably in an environment where one of their most essential inputs has become one of their greatest financial risks?

Fertilizer is not optional

For many industries, rising resource prices can be addressed by reducing consumption or switching suppliers.

Agriculture operates differently.

Fertilizer is not simply another operating expense. It is one of the core biological drivers of production itself. According to the USDA Economic Research Service, fertilizer represented between 33-44% of corn operating costs and 34-45% of wheat operating costs between 2020 and recent production years [7].

This makes nitrogen one of the largest and least avoidable operational expenses on many farms.

And importantly, fertilizer costs do not exist in isolation. They compete directly with every other critical investment required to keep a farming business operational: machinery, fuel, labor, financing, land, repairs, chemicals, and day-to-day operational maintenance.

This is what makes fertilizer inflation so economically dangerous. When nitrogen prices rise sharply, the pressure does not remain limited to the fertilizer budget alone. It spreads across the entire financial structure of the farm. Capital that would otherwise be invested into equipment upgrades, modernization, workforce expansion, or operational resilience is increasingly redirected toward securing enough fertilizer to protect yield potential.

Can farms switch fertilizers?

The reality of nitrogen fertilization is far more complex than simply “switching products.”

Nitrogen itself is not a single product category.

At the broadest level, agriculture relies on two major sources of nitrogen: organic and mineral fertilizers.

Organic sources include manure, crop residues, and other biological residuals that naturally return nutrients to the soil. These inputs play an important role in nutrient cycling and soil health. However, one of their biggest limitations is variability. The exact nitrogen availability from organic fertilizers can be difficult to predict, as nutrient release depends heavily on decomposition rates, soil biology, moisture, and temperature conditions.

Mineral fertilizers, by contrast, are designed to provide more concentrated and measurable nutrient delivery. And globally, the nitrogen fertilizer market is dominated by only a few major product categories.

Globally the market remains overwhelmingly dependent on a small number of mineral nitrogen products.

According to International Fertilizer Association (IFA) consumption data on a nitrogen nutrient basis, urea remains by far the dominant nitrogen fertilizer worldwide. Containing approximately 46% nitrogen, urea is the most concentrated solid nitrogen fertilizer and accounted for approximately 78% of global apparent nitrogen fertilizer consumption in 2023 [8].

The second-largest category is ammonium nitrate (AN), valued for its rapid nitrogen availability and lower volatilization risk compared to surface-applied urea. In 2023, ammonium nitrate represented approximately 13% of global apparent nitrogen fertilizer consumption according to IFA data [8].

Ammonium sulfate (AS), which supplies both nitrogen and sulfur, accounted for approximately 6% of global apparent nitrogen fertilizer consumption. The product is particularly important in sulfur-deficient soils and in regions where sulfur nutrition has become increasingly critical for crop performance [8].

The dominance of urea is not accidental.

Containing approximately 46% nitrogen, urea offers extremely high nutrient concentration relative to transport cost. In regions such as Latin America, Africa, and large parts of Asia, granular urea remains economically attractive partly because it is easier and cheaper to transport compared to many nitrate-based fertilizers.

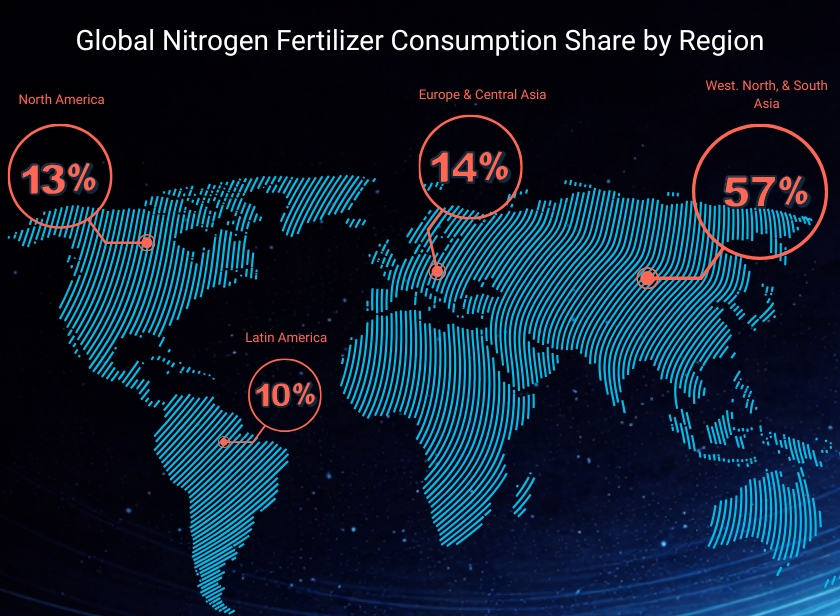

Regional consumption patterns also differ significantly. According to IFA data, approximately 57% of global nitrogen fertilizer consumption takes place in Asia, while Latin America represents roughly 10% of global nitrogen demand [8].

Crop structure further shapes fertilizer demand. Brazil, for example, consumes large volumes of phosphate and potash fertilizers due to extensive soybean production, while soybean crop rotations also biologically fix nitrogen, partially reducing mineral nitrogen dependence.

In theory, farms can explore alternative fertilizers, biologicals, or nutrient strategies.

In practice, however, the combination of infrastructure, logistics, agronomic familiarity, and market dependence makes rapid replacement extremely difficult.

So if farms cannot fully replace nitrogen, what else can they do?

The hidden cost of expensive fertilizer

One of the most misunderstood aspects of fertilizer inflation is this: rising fertilizer prices do not reduce fertilizer demand, because farmers understand the risk.

Reducing nitrogen application may lower costs in the short term but it may also reduce yield, lower grain quality, and threaten overall profitability.

As a result, farms rarely respond to fertilizer inflation by immediately cutting nitrogen application altogether. The risk to yield and therefore to overall profitability is often considered too high.

Instead, the financial pressure spreads across the broader operation. Many farms postpone machinery purchases, delay modernization projects, reduce labor costs, defer equipment repairs, or scale back acreage. Others shift toward less fertilizer-intensive crops or operate under significantly tighter margins while increasing exposure to operational debt.

In practice, expensive fertilizer does not only affect nutrient management decisions. It reshapes the entire economic structure of the farm and can slow long-term investment, innovation, and operational resilience across the agricultural sector.

This creates a hidden secondary effect of fertilizer inflation: high fertilizer prices can slow overall farm modernization and investment capacity.

Research already shows farms adapting in exactly these ways. According to analysis published in Choices Magazine, high fertilizer prices have incentivized growers to reduce planted acreage, shift toward crops requiring lower nitrogen input and adopt conservation practices such as cover crops and diversified crop rotations to improve soil fertility naturally [9].

Reuters also reported that U.S. farmers are expected to reduce corn acreage partly due to sustained fertilizer pressure, while some producers may reduce phosphate applications where residual soil nutrients allow temporary reductions. Nitrogen, however, remains far more difficult to postpone because crops depend on it immediately for growth [10].

The American Farm Bureau Federation similarly warned that when growers cannot afford full fertilizer application rates, reduced nutrient use increases the risk of lower yields and reduced production potential [3].

This is why the fertilizer crisis becomes far larger than a pricing issue.

It reshapes the entire economic structure of the farm.

A different strategy: efficiency instead of reduction

At first glance, rising input costs create an intuitive response: cut spending.

But agriculture has another option. Instead of simply reducing inputs, farms can increase efficiency, reduce waste, and improve return on investment from every unit applied. And this changes the conversation completely.

Because the goal is no longer: “How do we survive using less?”

The goal becomes: “How do we produce more efficiently?”

This is where several important adaptation strategies emerge simultaneously:

- investing in enhanced-efficiency fertilizers

- using biologicals and stabilizers

- improving nutrient timing

- adopting conservation practices

- and increasingly, implementing precision agriculture technologies

The fertilizer industry itself is already moving in this direction.

Enhanced Efficiency Fertilizers (EEFs), slow-release fertilizers, nitrification inhibitors, urease inhibitors, biologicals, and controlled-release products are expanding rapidly as agriculture searches for ways to improve nitrogen use efficiency and reduce losses.

At the same time, technologies such as real-time soil analysis allow farms to optimize fertilizer application dynamically based on actual field conditions rather than generalized assumptions.

And this is where precision nutrient management becomes economically transformative.

Because precision agriculture does not only reduce fertilizer use.

It reduces pressure across the entire operational budget.

From cost reduction to operational resilience

The real power of precision nutrient management is not simply “saving fertilizer.”

It is creating operational flexibility.

By measuring plant-available nitrogen directly in the field and continuously adjusting fertilization strategies throughout the growing season, farms can:

- reduce unnecessary nitrogen application

- lower exposure to volatile fertilizer markets

- improve yield stability

- free up capital for other investments

And importantly, the impact extends far beyond immediate fertilizer savings alone. By reducing unnecessary nitrogen application and improving nutrient efficiency, farms can free up capital that would otherwise be absorbed by input costs and redirect it toward higher-efficiency technologies, biologicals, premium fertilizers, modernization, and broader operational improvements that may previously have seemed financially out of reach.

Over time, this creates a compounding effect across the entire farming operation: lower waste, higher nutrient efficiency, improved return on investment, stronger yield performance, and ultimately greater operational resilience in an increasingly volatile agricultural market.

Precision agriculture at system level

This is where Stenon’s technology becomes strategically important.

By enabling real-time, in-field measurement of plant-available nitrogen, Stenon allows farmers to optimize fertilization decisions dynamically across different growth stages and field conditions.

Instead of relying on static fertilizer plans or precautionary overapplication, growers can continuously adapt nitrogen strategies based on actual crop demand and soil variability.

The result is not simply reduced nitrogen input.

Across global case studies, Stenon has demonstrated that farms can:

✅ reduce nitrogen fertilizer usage

✅ maintain or improve yield

✅ improve ROI

✅ create budget space for advanced fertilizers, biologicals, and enhanced-efficiency products

In other words: precision agriculture allows farms not only to survive the fertilizer crisis but potentially to emerge from it more efficient and more profitable than before.

And the implications extend far beyond individual farms.

Higher fertilizer efficiency means more stable food production, reduced dependence on volatile global supply chains, lower environmental impact, and greater resilience against geopolitical and macroeconomic disruption.

Ultimately, the future of agriculture will not belong to the farms that simply buy more fertilizer.

It will belong to the farms that use every unit more intelligently.

Sources:

[1] Reuters (2026): India urea prices double to $1,000 in tender on Iran war shock. https://www.reuters.com/world/china/indian-potash-ltd-receives-higher-urea-offers-iran-conflict-tightens-supply-2026-04-15/

[2] Successful Farming (2025): Farm Bankruptcies This Year Already Exceed 2024 Levels. https://www.agriculture.com/partners-farm-bankruptcies-this-year-already-exceed-2024-levels-11772290

[3] Farm Bureau (2026): Farm Bureau Survey Reveals Real Impact of Fertilizer Availability and Price. https://www.fb.org/market-intel/farm-bureau-survey-reveals-real-impact-of-fertilizer-availability-and-price

[4] FAO Food Price Index (2026): FAO Food Price Index extends upward trend amid higher vegetable oil, meat and cereal prices. https://www.fao.org/worldfoodsituation/FoodPricesIndex/en/

[5] FAO (2026):FAO: Protracted Strait of Hormuz crisis could turn into global agrifood catastrophe. https://www.fao.org/newsroom/detail/fao–protracted-strait-of-hormuz-crisis-could-turn-into-global-agrifood-catastrophe/en

[6] Reuters (2026): World Bank forecasts 24% surge in energy prices in 2026 due to Middle East war. https://www.reuters.com/business/energy/world-bank-forecasts-24-surge-energy-prices-2026-due-middle-east-war-2026-04-28/

[7] Economic Research Service (2025): Fertilizer prices stable at onset of 2025 planting season, below highs of 2021 and 2022. https://www.ers.usda.gov/data-products/charts-of-note/chart-detail?chartId=111221

[8] International Fertilizer Association (2023): Fertilizer consumption. https://ifastat.org/fertilizer-reports-analysis/fertilizer-consumption

[9] Choices Magazine (2025): Impact of High Fertilizer Prices and Farmer’s Adaptation Strategies in the U.S. Midwest. https://www.choicesmagazine.org/choices-magazine/submitted-articles/impact-of-high-fertilizer-prices-and-farmers-adaptation-strategies-in-the-us-midwest

[10] Reuters (2026): Nutrien expects higher potash demand despite tough conditions. https://www.reuters.com/world/americas/nutrien-expects-higher-potash-demand-despite-tough-conditions-farmers-2026-02-19/

About Stenon

Since its founding in 2018, Stenon GmbH, based in Potsdam, Germany, has become the global market leader in real-time digital soil data that is especially beneficial for agricultural producers, consultants and precision agriculture businesses. With its sensor- and cloud-based mobile measuring device FarmLab, Stenon provides agriculture businesses with essential data to make optimal and sustainable cultivation decisions, boost yield, crop quality and soil health while saving money on inputs.